NBER Reporter 2012 Number 3: Research Summary

Understanding the Profitability of Currency-Trading Strategies

Craig Burnside, Martin Eichenbaum, and Sergio Rebelo *

The profitability of simple currency-trading strategies presents perhaps even more of a challenge to traditional asset-pricing theory than does the equity-premium puzzle, which has received an enormous amount of attention. Understanding the properties of currency-trading strategies is important not just for asset pricing but for macroeconomics more generally. It is widely believed that these strategies are partly responsible for the high volatility of international capital flows, which are often viewed as problematic by policymakers. Understanding the rationale for widely-used currency strategies is important for understanding exchange rate movements in general, as well as for assessing the normative and positive implications of capital flows.

In a series of papers, we have studied two widely-used currency strategies: carry trade and currency momentum. The carry-trade strategy consists of borrowing low-interest-rate currencies and lending high-interest-rate currencies. The currency-momentum strategy consists of going long (short) on currencies for which long positions have yielded positive (negative) returns in the recent past. One appealing property of these strategies is that a practitioner does not need to estimate any parameters to implement them. One could, of course, entertain more complex versions of these strategies that, for example, optimally weight different currencies, or introduce volatility triggers that reduce exposure at times of high volatility.

This summary reviews our research on these trading strategies. First, we describe the empirical properties of the payoffs to carry and momentum. Second, we discuss whether these payoffs can be viewed as a reward for exposure to conventional types of risk. Third, we explore the plausibility of peso-event-based explanations of the payoffs. Finally, we review our work emphasizing the importance of microstructure frictions and the behavioral biases in understanding currency trading strategies.

(pdf)

(pdf)

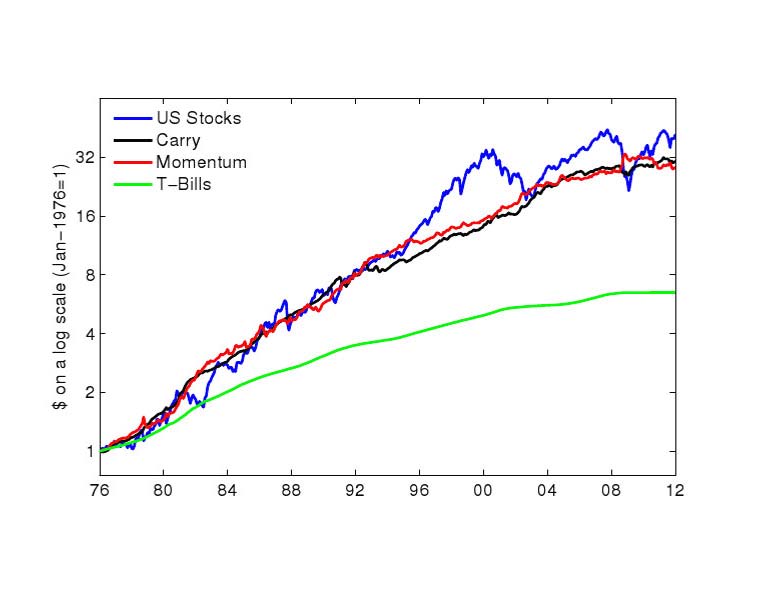

Figure 1

Properties of Payoffs to Carry and Momentum

As in all of our work, here we consider a carry-trade strategy that combines individual-currency carry trades into an equally-weighted portfolio. We use the same 20 currencies considered in Burnside, Eichenbaum and Rebelo (2011), henceforth BER (2011).1 The momentum strategy discussed below combines individual currency-momentum strategies into an equally-weighted portfolio of the same 20 currencies. We implement a monthly version of both strategies.2 All portfolios are constructed assuming that the U.S. dollar is the domestic currency.

Figure 1 displays the cumulative returns to investing in the carry and momentum strategies and in the U.S. stock market. The investment period spans March 1976 to January 2012.3 Two features of Figure 1 are worth noting. First, the cumulative returns to both strategies are almost as high as the cumulative return to investing in stocks. Second, the cumulative returns to the stock market are much more volatile than those of the currency portfolios.

The carry-trade strategy has an average annualized payoff of 4.5 percent, with a standard deviation of 5.2 percent, and a Sharpe ratio (the ratio of the mean excess return to its standard deviation) of 0.86. The momentum strategy is also highly profitable, yielding an average annualized payoff of 4.4 percent. The momentum payoffs have a standard deviation of 7.3 percent and a Sharpe ratio of 0.60.

The Sharpe ratios of both currency strategies are substantially higher than that of the stock market. The average excess return to the U.S. stock market over our sample period is 6.5 percent, with a standard deviation of 15.8 percent and a Sharpe ratio only equal to 0.41.

To an important degree, the high Sharpe ratio of the carry-trade strategy reflects the large gains from diversifying across carry-trade strategies for individual currencies (see Burnside, Eichenbaum, Kleshchelski, and Rebelo (2006), henceforth BEKR (2006)).4 In our sample, this diversification cuts the volatility of the payoffs by more than 50 percent. Since the average payoff is not affected, the Sharpe ratio of the portfolio doubles relative to the average Sharpe ratio of individual carry trades.5 Similar gains to diversification obtain for currency momentum.

Surprisingly, the payoffs to the carry and momentum strategies are roughly uncorrelated. So, from an investor standpoint, there are obvious gains to using both currency-trading strategies simultaneously. Even more striking is the fact that the payoffs to these strategies are uncorrelated with stock market returns. So, the currency-trading strategies provide a natural source of diversification when combined with a broad portfolio of U.S. stocks.

Are the returns to the carry and momentum strategies compensation for measurable risk?

The profitability of both currency strategies stems from the failure of uncovered interest rate parity (UIP). According to this condition, the rate of expected exchange rate depreciation of the domestic currency is equal to the difference between the domestic and the foreign interest rate. The empirical failure of this condition has been extensively documented (see for example Fama (1984) and Eichenbaum and Evans (1995)).6

The failure of UIP is not surprising from a theoretical perspective. For UIP to hold, agents must be risk neutral. So, a natural explanation for both the failure of UIP and the profitability of our currency trading strategies is the presence of a risk premium that compensates investors for the covariance between the payoffs to the currency strategies and their stochastic discount factor. In BEKR (2006), BER (2011), and Burnside, Eichenbaum, Kleshchelski, and Rebelo (2011), henceforth BEKR (2011),7 and in Burnside (2011), we argue that the profitability of these strategies is not a compensation for risk, at least as conventionally measured. Our basic argument is simple: the covariance between the payoffs to these two strategies and conventional risk factors is not statistically significant. Moreover, these risk factors leave unexplained economically large and statistically significant pricing errors. In the parlance of Wall Street, these strategies seem to generate high alphas.

The difficulty in explaining the profitability of the carry trade with conventional risk factors has led researchers such as Lustig, Roussanov, and Verdelhan (2011) and Menkhoff, Sarno, Schmeling, and Schrimpf (2012),8 to construct empirical risk factors specifically designed to price the average payoffs to portfolios of carry-trade strategies.

A natural question is whether these risk factors explain the profitability of the momentum strategy. BER (2011) argue that they don't. In particular, they find that the risk factor models proposed by Lustig et al. (2011) and Menkhoff et al. (2012) imply that momentum has a large, statistically significant alpha.

It is one thing to argue that stock and currency markets are segmented, so that we need currency-specific factors to price currency strategies. But, surely, factors that explain carry-trade payoffs should also explain the currency-momentum payoffs. Since they don't, we are skeptical that the profitability of the carry trade and momentum reflects exposure to observable risk factors.

One interesting possibility is that traders who specialize in these strategies are being compensated for the fact that payoffs are strongly negatively skewed. In fact, the carry trade is sometimes characterized as "picking up pennies in front of a truck." In BEKR (2011) and BER (2011), we find that the skewness of the carry-trade payoffs is statistically insignificant. Even if we take the point estimates of skewness at face value, the carry-trade payoffs are less skewed than the payoffs to the U.S. stock market. The payoffs to the momentum portfolio are actually positively skewed, though not significantly so. As far as fat tails are concerned, currency returns do display excess kurtosis, especially in the case of the carry-trade portfolio.

One way to illustrate the presence of fat tails in the payoffs generated by our strategies is to compute the worst in-sample annual payoffs to currency strategies. In our sample, the worst annual payoff is negative 5.6 percent for the carry trade (in 2008) and negative 10.9 percent for momentum (in 2012). It is important to keep these losses in perspective: the worst annual payoff to the U.S. stock market over our sample was negative 40 percent (in 2008). By this metric, the dangers associated with the fat tails of the currency strategies are much less pronounced than those associated with the stock market.

The relatively small fat tails of the currency payoffs reflect, in part, the gains from diversification. For example, the negative 5.6 percent payoff to the carry trade in 2008 masks great heterogeneity in the individual carry-trade payoffs. During that year, the payoffs to the carry trade of the U.S. dollar against the Norwegian krone or the New Zealand dollar were both roughly negative 20 percent. In contrast, the payoff to the carry trade of the U.S. dollar against the euro and the Danish krone were both roughly 14 percent.

One interesting question is whether the presence of fat tails would deter an investor from investing in the carry trade. To address this question, BEKR (2006) consider an investor with a coefficient of constant relative-risk-aversion equal to five. As it turns out, this investor would allocate 187 percent of his portfolio to the carry trade, 68 percent to stocks, and borrow 157 percent at the risk-free rate. These results are consistent with the notion that the carry trade is a bigger asset-pricing puzzle than the equity premium.

"Peso Problems"

An alternative explanation for the profitability of our two currency strategies is the possibility of rare disasters or "peso problems." By rare disasters, we mean very low probability events that sharply decrease the payoffs and/or sharply increase the value of the stochastic discount factor. These events may occur in sample. But, due to their low probability, they may be under-represented relative to their true frequency in population. As a result, a researcher would over-estimate the profitability of currency trading. By a "peso problem," we mean the effects on inference caused by the most extreme form of under-representation: the events do not occur in sample.

In BEKR (2011), we study the empirical plausibility of the peso-problem explanation by analyzing the payoffs to a version of the carry-trade strategy that does not yield high negative payoffs in a peso state. The strategy works as follows. When an investor borrows foreign currency, he simultaneously buys a call option on that currency with the same maturity as the foreign currency loan. If the foreign currency appreciates beyond the strike price, the investor can buy the foreign currency at the strike price and repay the loan.9 Similarly, when an investor lends in foreign currency, he can hedge the downside risk by buying a put option on the currency. By construction, this "hedged carry trade" is immune to large losses such as those potentially associated with a peso event.

BEKR (2011) use data on currency options to estimate the average risk-adjusted payoff to the hedged carry trade. They find that this payoff is smaller than the payoff to the unhedged carry trade. This finding is consistent with the view that the average payoff to the unhedged carry trade reflects a peso problem. An obvious question is: what is the nature of the peso event for which agents are being compensated?

It is useful to distinguish between two extreme possibilities. The first possibility is that the salient feature of a peso state is large carry-trade losses. The second possibility is that the salient feature of a peso state is a large value of the stochastic discount factor. BEKR (2011) find that a peso event reflects high values of the stochastic discount factor in the peso state rather than very large negative payoffs to the unhedged carry trade in that state.

The intuition for this result is as follows: any risk-adjusted payoffs associated with the carry trade in the non-peso states must, on average, be compensated, on a risk-adjusted basis, for losses in the peso state. According to our estimates, the average risk-adjusted payoffs of the hedged and unhedged carry trade in the non-peso states are not very different. Consequently, the risk-adjusted losses to these two strategies in the peso state cannot be very different. Since the value of the stochastic discount factor in the peso state is the same for both strategies, the actual losses of the two strategies in the peso state must be similar. By construction there is an upper bound to the losses of the hedged carry trade. This upper bound tells us how much the hedged carry-trade strategy loses in the peso state. Since these losses turn out to be small, the losses to the unhedged carry trade in the peso state must also be small.

The rationale for why the stochastic discount factor is much larger in the peso state than in the non-peso states is as follows. We just argued that the unhedged carry trade makes relatively small losses in the peso state. At the same time, the average risk-adjusted payoff to the unhedged carry trade in the non-peso states is large. The only way to rationalize these observations is for the stochastic discount factor to be very high in the peso state. So, even though the losses of the unhedged carry trade in the peso state are moderate, the investor attaches great importance to them.

In BER (2011), we use a similar approach to study an equally-weighted portfolio of carry trade and momentum strategies. Again, we find that the only way to rationalize the hedged and unhedged payoffs is to characterize the peso event as one that involves moderate losses but a high value of the stochastic discount factor.

It is worth emphasizing that the 2008 financial crisis is not an example of the kind of rare disaster that rationalizes the profitability of currency trading. The reason is simple: momentum made money during the financial crisis.

Microstructure Based Explanations of the Profitability of Currency Strategies

The peso event rationalization takes a very macroeconomic perspective of the risks to currency traders. In this section, we discuss our work that focuses on the microstructure of foreign exchange markets.

Macroeconomists generally assume that asset markets are Walrasian in nature. This assumption is highly questionable. The foreign exchange market is actually a decentralized, over-the-counter market in which market makers play a central role. In BER (2011 and 2009)10 , we explore the impact of two types of microstructure frictions that can potentially account for key anomalies in exchange rate markets.

BER (2011) explore the impact of price pressure in foreign exchange markets on the profitability of our currency-trading strategies. By price pressure we mean that the price at which investors can buy or sell currencies depends on the quantity they wish to transact. Price pressure introduces a wedge between marginal and average payoffs to a trading strategy. As a result, observed average payoffs can be positive even though the marginal trade is not profitable. So, traders do not increase their exposure to the strategy to the point where observed average risk-adjusted payoffs are zero.

Finally, BER (2009) study an adverse-selection model that rationalizes the failure of UIP. The key feature of the model economy studied in that paper is that the adverse selection problem facing market makers is worse when, based on public information, the currency is expected to appreciate. The model can rationalize the forward premium puzzle: a regression of the change in the exchange rate on the forward premium has a negative slope.11

Behavioral Explanations for the Forward Premium Puzzle

Burnside, Han, Hirshleifer, and Wang (2011)12 offer an alternative explanation for the forward premium puzzle in foreign exchange markets based upon investor overconfidence. In the most basic version of their model, a positive (bad) signal about U.S. inflation causes the U.S. dollar to depreciate in the spot market. It depreciates even more in the forward market because expected future U.S. dollar depreciation is associated with the positive inflationary signal. Given agents' overconfidence, however, both the spot rate and the forward rate tend to overshoot their long-run level. So, when agents observe a signal of higher future inflation, the consequent rise in the forward premium predicts a subsequent downward correction of the spot rate. The model can explain the forward premium puzzle and several other stylized facts related to the joint behavior of forward and spot exchange rates. It is also consistent with the availability of profitable carry-trade strategies. Versions of the model that incorporate New Keynesian frictions can, additionally, rationalize both the forward-premium puzzle and the observation that bad signals about U.S. inflation are often associated with U.S. dollar appreciation, rather than depreciation (see Andersen et al., 2003 and Clarida and Waldman, 2008).13

Concluding Remarks

In this note, we have reviewed our work on currency-trading strategies. We view this work as fitting into a broader research agenda of incorporating realistic financial frictions into modern macro models. A critical component of this agenda will involve asking who is on the other side of common trading strategies and why. We suspect that the answer will inevitably involve heterogeneity in expectations and persistent disagreement among agents. Allowing for these elements requires fundamental changes in mainstream macro models. For some recent steps in this directions see, for example, Acemoglu, Chernozhukov and Yildiz (2009), Angeletos and La'O (2011), Brunnermeier and Wei Xiong, (2012), Simsek (2012), and Burnside, Eichenbaum and Rebelo (2012).14

* Burnside, Eichenbaum, and Rebelo are Research Associates in the NBER's Program on Economic Fluctuations and Growth.

1. The countries included in our sample are: Australia, Austria, Belgium, Canada, Denmark, France, Germany, Ireland, Italy, Japan, the Netherlands, New Zealand, Norway, Portugal, South Africa, Spain, Sweden, Switzerland, the United Kingdom, and the United States.

2. For the momentum strategy, we use returns obtained in the previous month to decide whether to go long or short on the currency. See C. Burnside, M.S. Eichenbaum, and S. Rebelo, "Carry Trade and Momentum in Currency Markets," NBER Working Paper No. 16942, April 2011, and Annual Review of Financial Economics, 3, December 2011, pp. 511-35.

3. Since the currency strategies involve zero net investment, we compute the cumulative payoffs as follows: we initially deposit one U.S. dollar in a bank account that yields the same rate of return as the Treasury bill rate. In the beginning of every period, we bet the balance of the bank account on the strategy. At the end of the period, payoffs to the strategy are deposited into the bank account.

4. C. Burnside, M.S. Eichenbaum, I. Kleshchelski, and S. Rebelo, "The Returns to Currency Speculation," NBER Working Paper No. 12489, August 2006.

5. See C. Burnside, M.S. Eichenbaum, and S. Rebelo, "Carry Trade: the Gains from Diversification," Journal of the European Economic Association, 6(2-3), April-May 2008, pp. 581–8. They show that similar diversification effects hold for carry-strategies implemented with emerging market currencies.

6. In fact, Burnside, Eichenbaum, Kleshchelski, and Rebelo (2006) show that currency-trading strategies that use the interest rate differential to forecast the returns for going long in a particular currency have lower Sharpe ratios than the carry trade. See E. Fama, "Forward and spot exchange rates," Journal of Monetary Economics, Volume 14, Issue 3, November 1984, pp.319–38, and M. Eichenbaum and C. Evans "Some Empirical Evidence on the Effects of Shocks to Monetary Policy on Exchange Rates," NBER Working Paper No. 4271, February 1993, The Quarterly Journal of Economics (1995) 110(4): pp. 975-1009.

7. C. Burnside, M.S. Eichenbaum, I. Kleshchelski, and S. Rebelo, "Do Peso Problems Explain the Returns to the Carry Trade?" NBER Working Paper No. 14054, June 2008, and Review of Financial Studies, 24(3), March 2011, pp. 853-91, and C. Burnside, "Carry Trades and Risk," NBER Working Paper No. 17278, August 2011, and in Handbook of Exchange Rates, J. James, I.W. Marsh, and L. Sarno, eds. (Hoboken: John Wiley & Sons, 2012) pp. 283-312.

8. H. Lustig, N. Roussanov, and A. Verdelhan, "Common Risk Factors in Currency Markets," NBER Working Paper No. 14082, June 2008, and Review of Financial Studies, 24(11), November 2011, pp. 3731-77, and L. Menkhoff, L. Sarno, M. Schmeling, and A. Schrimpf, "Currency Momentum Strategies," Journal of Financial Economics, forthcoming.

9. It is possible that the counterparty in the options would default in the peso event. However, investors use options traded in exchanges to hedge. Since these contracts are marked to market on a daily basis, the risk of a default appears to be quite small at a practical level.

10. C. Burnside, M.S. Eichenbaum, and S. Rebelo, "Understanding the Forward Premium Puzzle: A Microstructure Approach," NBER Working Paper No. 13278, July 2007, and American Economic Journal: Macroeconomics, 1(2), July 2009, pp. 127-54.

11. The forward premium is the percentage difference between the forward rate and the spot exchange rate.

12. C. Burnside, B. Han, D. Hirshleifer, and T.Y. Wang, "Investor Overconfidence and the Forward Premium Puzzle," NBER Working Paper No. 15866, April 2010, and Review of Economic Studies, 78(2), April 2011, pp. 523-58.

13. T.G. Andersen, T. Bollerslev, F. Diebold, and C. Vega, "Micro Effects of Macro Announcements: Real-time Price Discovery in Foreign Exchange," NBER Working Paper No. 8959, May 2002, and American Economic Review, 93, March 2003, pp. 38-62, and R. Clarida and D. Waldman, "Is Bad News about Inflation Good News for the Exchange Rate? And, If So, Can That Tell Us Anything about the Conduct of Monetary Policy?" NBER Working Paper No. 13010, April 2007, and in Asset Prices and Monetary Policy, J.Y. Campbell, ed. (Chicago: University of Chicago Press, 2008), pp. 371–92.

14. D. Acemoglu, V. Chernozhukov, and M. Yildiz, "Fragility of Asymptotic Agreement under Bayesian Learning," MIT Working Paper No. 08-09, February 2009; G-M. Angeletos and J. La'O, "Optimal Monetary Policy with Information Frictions," NBER Working Paper No. 17525, November 2011; M.K. Brunnermeier and Xiong Wei, "A Welfare Criterion for Models with Heterogeneous Beliefs," Working Paper, October 2011; and A. Simsek, "Belief Disagreement and Collateral Constraints," Working Paper, March 2012.