|

|

|

|

|

Transfer Payments and the Macroeconomy

"...different responses of monetary policy to benefit increases and tax cuts probably explain their very different macroeconomic effects."

Christina Romer and

David Romer examine the macroeconomic effects of changes in Social Security benefits in the United States from 1952 to 1991 in their paper Transfer Payments and the Macroeconomy: The Effects of Social Security Benefit Changes, 1952-1991 (NBER Working Paper No. 20087).

During this period, increases in Social Security benefits varied widely in size and timing, and were only rarely implemented in response to short-run macroeconomic developments. As a result, these benefit increases can be used to estimate the short-run macroeconomic effects of changes in transfer payments.

The researchers focus primarily on aggregate consumer spending as a measure of macroeconomic activity. Their estimates suggest a large and immediate spending response following a permanent increase in benefits. In the month of a permanent benefit increase, there is a nearly one-for-one rise in consumer spending. This effect persists for roughly half a year, and then sharply diminishes. Temporary benefit changes, on the other hand, have a much smaller impact on consumption. Broader measures of economic activity, such as industrial production or employment, do not appear to respond to changes in benefits, whether permanent or temporary.

The authors also compare the effects of changes in taxes and transfers on consumption, testing the prediction of Keynesian models in which taxes and transfers have equal and opposite effects on household consumption and overall economic activity. They find that the initial consumption impact of a tax cut is smaller than that of a transfer increase, but that the response to the tax cut rises steadily and persistently. Overall, tax cuts have a much larger impact on consumption than benefit increases. Because their effects on consumption are more persistent, tax changes, unlike benefit changes, do affect broader economic indicators.

What explains the differential response of the economy to these two types of fiscal changes? The researchers suggest that the different responses of monetary policy to benefit increases and tax cuts probably explain their very different macroeconomic effects. The federal funds rate rises sharply and significantly after permanent Social Security benefit increases, but it moves very little, and on average may decline, during the year following tax cuts. Narrative evidence from Federal Reserve records confirms that monetary policymakers regard increases in Social Security benefits as expansionary, and therefore call for tighter monetary policy in response. This feature of the monetary policy reaction could explain both the lower persistence of the consumption effects of Social Security benefit increases, and the absence of an effect on broader indicators of economic activity when these benefits change. In contrast, monetary policymakers were much less consistent in advocating for monetary policy changes that would counteract the likely effects of tax changes on aggregate demand.

-- Claire Brunel

|

|

Do ETFs Increase Stock Volatility?

"...ETF ownership of stocks leads to higher volatility and turnover."

In recent decades, exchange-traded funds (ETFs) have grown rapidly. There has been little analysis of whether or how this development may affect the performance of securities markets. In Do ETFs Increase Volatility? (NBER Working Paper No. 20071),

Itzhak Ben-David,

Francesco Franzoni, and

Rabih Moussawi discover that the stocks that are held within such funds experience substantially higher intraday and daily volatility than stocks without substantial ETF holdings. The authors suggest that the arbitrage between ETFs and their underlying securities adds a whole new layer of trading to stocks that are held within ETFs, and fosters the propagation of trading shocks that occur in the ETF market. As a result, the non-fundamental volatility of the underlying securities increases.

ETFs are investment funds that typically focus on holding securities in specific asset classes, industries, or geographical areas. They are similar to passive index funds but they are individually listed on exchanges and can be traded daily by retail and institutional investors. New ETF shares can be created and redeemed on a continuous basis. ETFs were first introduced in the 1980s. They began to gain popularity in the 1990s and have experienced explosive growth since the turn of the century. By 2012, there were more than 1,600 ETFs worldwide, and at the end of 2013 these funds had more than $2.5 trillion of assets under management. At one point in 2010, exchange-traded products accounted for 40 percent of all trading volume in U.S. securities markets.

To study how ETFs affect securities markets, the authors combine data from the Center for Research in Security Prices, Compustat, Bloomberg, OptionMetrics, and Form 13F filings. They focus on a sample of ETFs that hold U.S. stocks and that were listed on U.S. exchanges over the period 2000 to 2012. The researchers use variations in ETF ownership of different stocks, and variation in the divergence between the prices of ETFs and their associated baskets of underlying securities, as well as associated fund flows, to explore the effects of ETF ownership on volatility. In addition, they exploit the fact that ETF ownership of a stock changes exogenously if that stock switches between being included in the Russell 2000 and Russell 1000 indexes. Their key finding is that ETF ownership of stocks leads to higher volatility and turnover. A one-standard-deviation increase in ETF ownership raises daily volatility and turnover by about 16 percent. Since much of the variation they study in ETF ownership of stocks is arguably independent of the inherent volatility of the stocks, the authors conclude that rising ETF ownership affects volatility.

The research suggests that the more the prices of ETFs and the prices of their underlying component securities diverge, and hence the greater the potential returns to arbitrage trades between the two, the greater the turnover and volatility of the stocks held in the ETF. The authors also find that increased stock volatility results from the flows into and out of ETFs. The price impact of ETF arbitrage appears to decay after a few days, which is consistent with ETFs adding noise to security prices.

-- Jay Fitzgerald

|

|

Patent Expiration and Pharmaceutical Prices

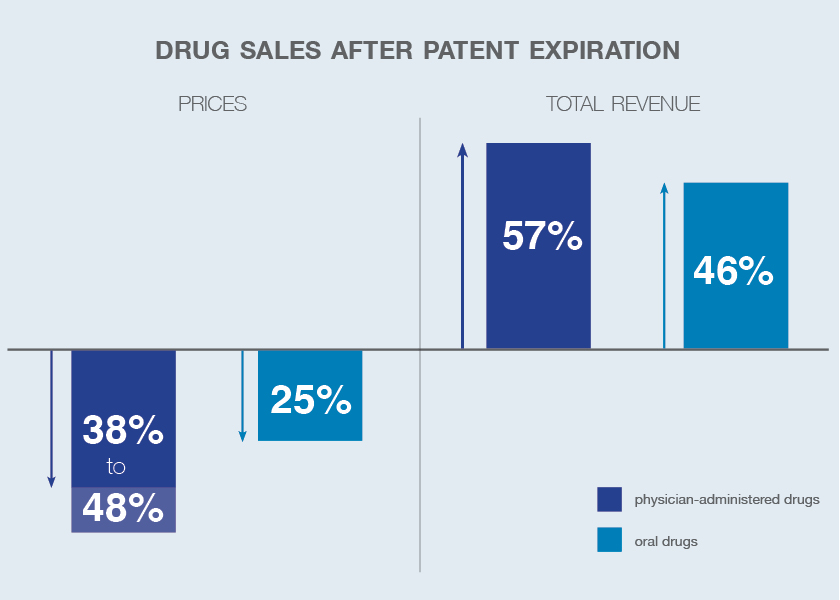

"The average price of physician-administered drugs declined by between 38 and 48 percent following patent expiration."

When a drug's U.S. patent expires, manufacturers other than the initial developer may take advantage of an abbreviated approval process to introduce lower-priced generic versions. In most uses, generics are clinically equivalent to the original branded drug. Some drugs are straightforward to imitate and produce at low cost. Others, particularly those requiring sterile manufacturing conditions or similarly complex production processes, are much more costly to copy.

In Specialty Drug Prices and Utilization after Loss of U.S. Patent Exclusivity, 2001-2007 (NBER Working Paper No. 20016),

Rena Conti and

Ernst Berndt use information from the IMS Health National Sales Perspectives database to study how generic introductions affected the pricing, sales, and use of the 41 cancer-related specialty drugs that lost patent protection between 2001 and 2007.

The authors find clear evidence that competitors entered the market and prices fell after patent expiration. Typically, between three and five manufacturers applied to produce generic versions of complex-to-manufacture physician-administered drugs. There were more applicants, 6.3 on average, for oral drugs. Average drug prices dropped after expiration. The average price of physician-administered drugs declined by between 38 and 48 percent following patent expiration. The decline was more modest, about 25 percent, for oral drugs. For these drugs after generic entry, high and increasing brand prices partly offset low and decreasing generic prices. Sales volume appears to increase substantially following generic entry, consistent with the usual assumptions regarding the negative relationship between prices and quantity demanded. As a result, total revenue from sales of both categories of drugs increased after patent expiration. For physician-administered drugs, the average increase in total revenue was 57 percent, while for oral drugs the increase was 46 percent.

-- Linda Gorman

|

|

Transfer Taxes and the Real Estate Market

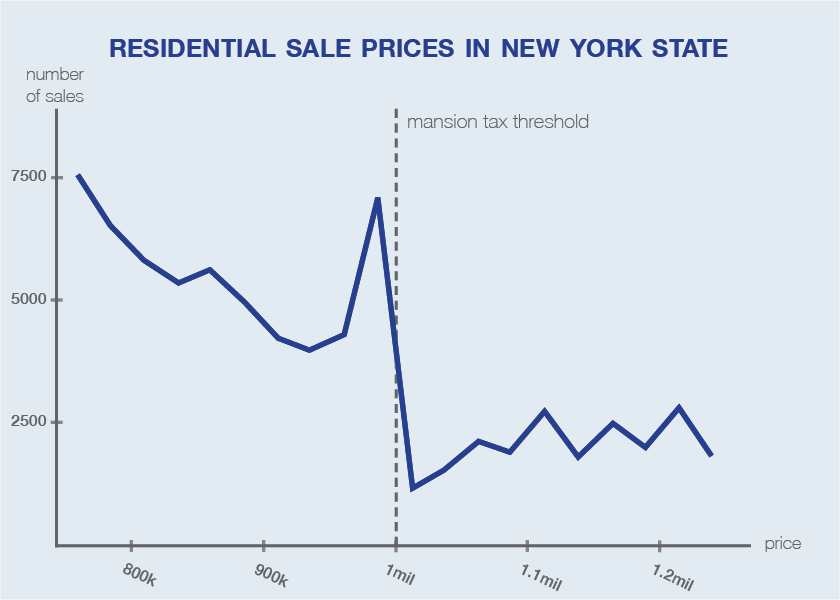

"...sales data show a substantial bunching of transactions right below the $1 million level."

New York City levies a "mansion tax" on real estate transactions that exceed $1 million in value. In Mansion Tax: The Effect of Transfer Taxes on the Residential Real Estate Market (NBER Working Paper No. 20084),

Wojciech Kopczuk and

David Munroe study the impact of these taxes on real estate transaction prices and the level of trading volume around tax thresholds. They study housing market data from both New York and New Jersey, which also levies a transaction tax, and find evidence that the taxes disrupt residential sales at the price point at which they take effect. Some sellers apparently reduce their transaction prices so that they fall below the threshold, and others choose not to sell at all.

In New York City, if a property sells for $999,999, no mansion tax is due, but if it sells for $1 million, the tax due is $10,000. This represents a "notch" in the tax schedule: a small change in the value of the transaction can trigger a discrete increase in tax liability. Not surprisingly, sales data show a substantial bunching of transactions right below the $1 million level. They also show "missing sales" just above the $1 million level. Relative to the number of transactions one would predict just above this threshold based on the number of sales in other price ranges, there are too few sales. The authors estimate that there were 2,800 such missing transactions in New York between 2003 and 2011, equivalent to the number of transactions that would have occurred otherwise in the price range of $1 million to $1.04 million. They conjecture that in some cases, if a property would sell for just over $1 million, the sellers may take it off the market or delay the sale, perhaps by renting. The authors conclude that "this one percent tax, applying at a relatively large threshold, managed to eliminate 0.7% of transactions."

The results suggest that the tax may distort market prices by more than the tax due. For example, it appears that even though the tax on a $1 million property is $10,000, some sellers may offer up to $20,000 in discounts to avoid the tax. The authors also emphasize that the tax has an "unraveling effect." They write that "the notched design of the tax can destroy a market for housing with values close to the notch." When potential taxpayers have the option of not participating in a market, as they can in the real estate market by not offering their property for sale, a notched transaction tax can destroy productive matches between potential buyers and potential sellers.

-- Laurent Belsie

|

|

Spatial Mismatch and the Duration of Joblessness

"...better job accessibility significantly decreases the duration of joblessness among lower-paid displaced workers."

Urban concentrations of lower-income and minority populations have higher than average unemployment rates. The spatial mismatch hypothesis (SMH) postulates that a worker with locally inferior job access is likely to experience worse labor market outcomes. If it is correct, then improving spatial access to jobs could lead to better employment outcomes. This logic has inspired urban planning policies aimed at moving jobs closer to neighborhoods with high unemployment, such as Employment Zones, as well as efforts to enhance transportation links between high unemployment neighborhoods and locations with an abundance of jobs. It also underpins proposals to relocate residents of high unemployment neighborhoods to job-abundant neighborhoods, for example, with a housing voucher program.

In Job Displacement and the Duration of Joblessness: The Role of Spatial Mismatch (NBER Working Paper No. 20066), authors

Fredrik Andersson,

John Haltiwanger,

Mark Kutzbach,

Henry Pollakowski, and

Daniel Weinberg study spatial mismatch by combining information from several data sources to generate improved person- and location-specific measures of job accessibility. They focus on workers displaced in mass layoffs, and investigate whether the job search duration after such a layoff is related to accessibility to appropriate jobs. This project exploits rich, matched employer-employee administrative data on job histories and search outcomes, as well as data on worker characteristics and neighborhood data from the decennial census, and comprehensive transportation network data from nine large Great Lakes metropolitan areas.

The authors find that better job accessibility significantly decreases the duration of joblessness among lower-paid displaced workers. In the center of the job accessibility distribution, an increase from the 25th to the 75th percentile of job accessibility is associated with a 4.2 percent reduction in search duration for finding any job, and a 5.6 (7.0) percent reduction for accessions to new jobs with pay equal to 75 (90) percent of prior job earnings, respectively. While job accessibility is only one of many factors affecting job search outcomes, it appears to play an especially important role for black workers, for women, and for older workers.

---Les Picker

|

|

Measuring Credit Risk in the Euro Area

"...credit spread indexes are strong predictors of future economic activity and of the growth in bank lending."

Measuring the extent of financial distress for countries within the European financial system is a difficult challenge. In Credit Risk in the Euro Area (NBER Working Paper No. 20041),

Simon Gilchrist and

Benoît Mojon develop new indexes of credit risks in the euro area. They analyze information on hundreds of thousands of monthly observations on the yield to maturity of corporate bonds since the launch of the euro in January 1999, and define the credit spread at the bond level as the difference between the corporate bond yield and the yield of a same-maturity German Bund zero coupon bond. They aggregate these bond-level credit spreads to obtain indexes of credit risk for both banks and non-financial corporations in Germany, France, Italy, and Spain, as well as for the entire euro area. The authors find that the financial crisis of 2008 dramatically increased the cost of market funding for both financial and non-financial firms in the euro area. In addition, coincident with the rise in sovereign default risk in the euro system, they find increasing fragmentation of the European financial system along national lines since 2010.

They also determine that their credit spread indexes are strong predictors of future economic activity and of the growth in bank lending. They are predictive of industrial production, unemployment, and real GDP both at the country level and for the entire euro area. These findings underscore the real consequences of deterioration in financial conditions.

--Matt Nesvisky

|

|

|

|

|

|

|

|

If you wish to unsubscribe from this email, please click here

Questions or problems with this email please contact: info@nber.org |

|

|

| The Digest is not copyrighted and may be reproduced freely with appropriate attribution of source. |

|